Understanding GST on Construction Materials in India 2026

The Goods and Services Tax (GST) regime has fundamentally transformed how construction materials are taxed in India since its implementation in 2017. As we move into 2026, it's crucial for architects, engineers, contractors, and construction professionals to have a clear understanding of the current GST structure on construction materials. Whether you're planning a residential project in Bangalore, a commercial complex in Mumbai, or an infrastructure development in Delhi, GST implications directly affect your project budget and profitability.

The GST framework for construction materials is complex and varies significantly based on the nature of materials, their processing stage, and their application. This comprehensive guide will help you navigate the GST landscape for construction materials in 2026 and ensure your projects remain compliant while optimizing costs.

Build cost · Bengaluru, May 2026

Current GST Rates on Construction Materials

The Five-Tier GST Structure

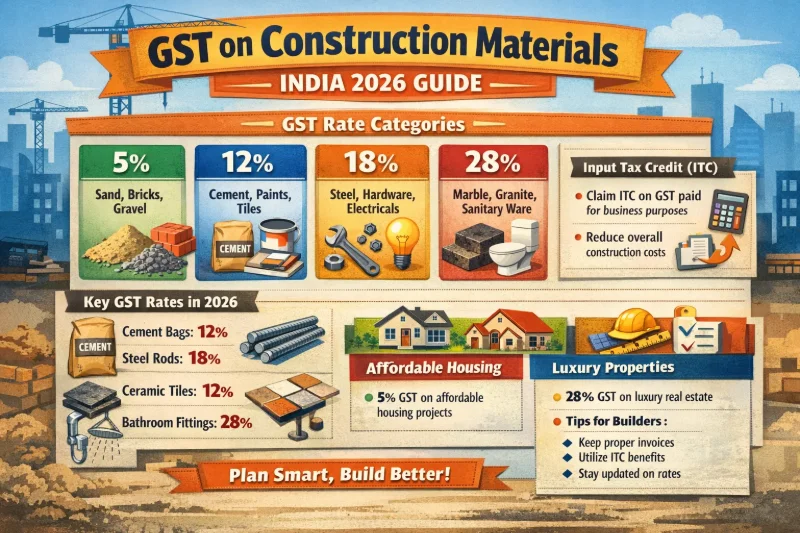

India's GST system operates on a five-tier tax structure: 0%, 5%, 12%, 18%, and 28%. Construction materials fall across different slabs depending on their nature and level of processing. Understanding these categories is essential for accurate project costing and compliance.

0% GST (Nil Rate): Certain raw materials and basic construction inputs attract zero GST. This includes items like raw minerals in their natural state, which are then processed into usable construction materials.

5% GST: This is the most beneficial rate for construction professionals. Many essential materials fall under this bracket, including cement, bricks, tiles, and certain steel products. The 5% rate applies to goods that are considered essential for construction and are typically used by lower-income groups.

12% GST: A significant portion of construction materials attracts 12% GST. This includes items like paints, varnishes, electrical fixtures, plumbing materials, and certain types of steel products.

18% GST: Premium and processed construction materials often fall under this category. This includes items like glass, certain types of tiles, decorative materials, and some specialized equipment.

28% GST: The highest rate applies to luxury items and specific goods like air conditioning equipment and certain electrical appliances used in construction.

Specific GST Rates for Common Construction Materials

Frequently asked

Cement and Concrete Products

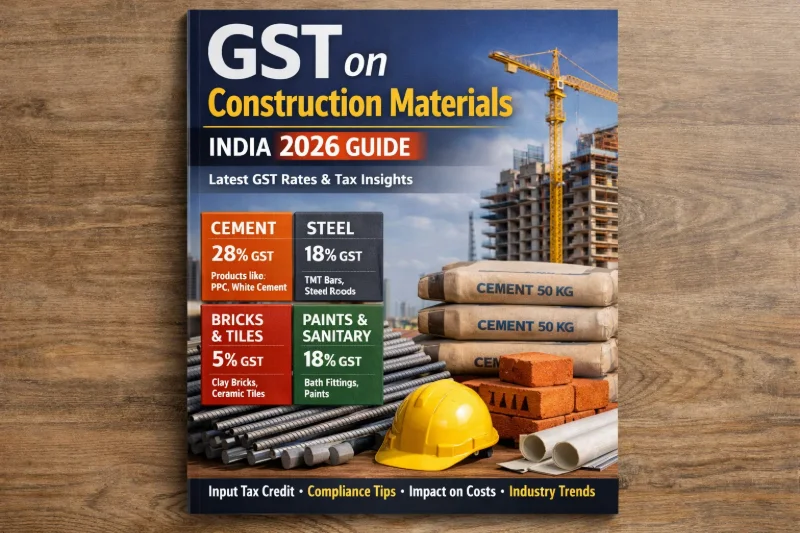

Cement is the backbone of Indian construction, and its GST treatment is favorable for the industry. Ordinary Portland Cement (OPC) and Portland Pozzolana Cement (PPC) attract 5% GST. This reduced rate recognizes cement's essential role in construction. Ready-mix concrete (RMC) also falls under the 5% bracket, making it an economical choice for large projects in cities like Pune, Hyderabad, and Kolkata.

For a typical construction project consuming 300-400 bags of cement per 1000 sq ft, the GST advantage of 5% versus a higher rate can mean significant savings. For example, at ₹500 per bag, the GST difference between 5% and 12% on 1000 bags amounts to ₹3,500—a substantial sum for medium-sized projects.

Steel and Iron Products

Steel is another critical material, and its GST classification depends on the processing stage and type. Mild steel bars and reinforcement steel (rebar) attract 5% GST, making them affordable for structural work. However, finished steel products, structural steel sections, and specialized steel items attract 12% GST.

This differentiation is important for project planning. If you're sourcing raw steel bars versus fabricated steel sections, your GST liability will differ. Many contractors in India prefer to source raw materials and handle fabrication in-house to optimize GST benefits, though this requires proper accounting and documentation.

Bricks and Masonry Materials

Bricks, whether clay or concrete, attract 5% GST. This includes hollow blocks and interlocking bricks used extensively in Indian construction. Given that a typical house requires 4,000-5,000 bricks, the 5% rate significantly impacts project economics.

Mortar and adhesive materials used with bricks generally attract 12% GST, so careful procurement planning is necessary. In metro cities like Chennai and Bangalore, where construction costs are high, every percentage point of GST matters for competitiveness.

Tiles and Flooring Materials

Ceramic tiles and vitrified tiles used for flooring and wall finishing attract 5% GST when they're basic utility tiles. However, decorative tiles, marble, granite, and premium flooring materials attract 12% or 18% GST depending on their nature and processing level.

This creates a clear cost incentive for using standard tiles over premium options. A project using 2,000 sq ft of tiles at ₹50 per sq ft would save ₹5,000 in GST by choosing 5% rated tiles over 12% rated ones.

Paints, Varnishes, and Coatings

Paints and varnishes attract 12% GST. This category includes interior and exterior paints, primers, and protective coatings. Given that painting is typically 3-5% of total construction costs, the 12% GST is a fixed expense that contractors must budget for carefully.

Electrical and Plumbing Materials

The GST on electrical and plumbing materials varies:

Basic electrical wires and cables: 12% GST

Switches, sockets, and fixtures: 12% GST

PVC pipes and fittings: 12% GST

Sanitaryware (toilets, basins): 12% GST

Taps and valves: 12% GST

For a typical residential project, electrical and plumbing materials might constitute 8-10% of total material costs. At ₹2,00,000 for these materials in a ₹25 lakh project, the 12% GST adds ₹24,000 to the cost.

Glass and Glazing Materials

Float glass and ordinary glass attract 12% GST, while tempered glass and specialized glass products attract 18% GST. This distinction is important for architects specifying materials. A building with extensive glazing in Delhi or Gurgaon will have significant GST implications based on glass specifications.

GST Impact on Construction Contracts and Project Costing

Input Tax Credit (ITC) Mechanism

One of the most important aspects of GST for construction professionals is the Input Tax Credit (ITC) mechanism. If you're a registered contractor or builder, you can claim credit for GST paid on materials and services used in your project. This significantly reduces your effective GST liability.

For example, if you purchase materials worth ₹100 lakhs with 5% GST (₹5 lakhs), and your output is taxed at 5% (₹5 lakhs on ₹100 lakhs of services), you can claim credit for the ₹5 lakhs paid on materials, resulting in zero net GST liability.

However, ITC is only available if:

You are registered under GST

Your suppliers are registered under GST

You have valid tax invoices from suppliers

The materials are used for taxable supplies

This is why it's critical to ensure all suppliers in your supply chain are GST registered. When sourcing materials from AECORD or other platforms, always verify supplier registration status.

Reverse Charge Mechanism

Under certain conditions, the recipient of goods or services must pay GST instead of the supplier. This reverse charge applies when:

Purchasing materials from unregistered suppliers above certain thresholds

Receiving services from unregistered service providers

Importing goods from outside India

For construction projects, this is particularly relevant when sourcing materials from small suppliers or informal sectors. Understanding when reverse charge applies helps in proper GST accounting and prevents compliance issues.

GST on Construction Services vs. Materials

Differential Treatment of Services

It's important to distinguish between GST on materials and GST on construction services. Construction services (labor, design, supervision) attract 5% or 12% GST depending on the project value and nature.

For projects below ₹50 lakhs, construction services typically attract 5% GST. Above ₹50 lakhs, they attract 12% GST. This creates an interesting dynamic in project budgeting. A ₹50 lakh project just under the threshold has significantly lower service GST than one slightly above it.

When you engage contractors or consultants through AECORD, ensure you understand the GST implications of their service charges and factor them into your project budget accordingly.

State-Specific Considerations and Compliance

Intra-State vs. Inter-State Supplies

GST is divided into CGST (Central GST) and SGST (State GST) for intra-state transactions, or IGST (Integrated GST) for inter-state transactions. For construction materials sourced within your state (e.g., cement from a supplier in Maharashtra for a project in Maharashtra), you pay CGST and SGST.

For materials sourced from other states, IGST applies. The total rate remains the same (5%, 12%, 18%, or 28%), but the distribution changes. This affects ITC claims and accounting procedures.

City-Specific Impacts

Different Indian cities have varying construction material availability and supplier bases. In metros like Delhi, Mumbai, and Bangalore, GST-registered suppliers are abundant, making ITC claims easier. In smaller cities like Jaipur, Lucknow, or Nagpur, the supplier base might include more unregistered vendors, complicating GST compliance.

When planning projects across different regions, account for these compliance variations in your project timeline and budget.

Recent Changes and Future Outlook for 2026

GST Council Decisions and Rate Changes

The GST Council periodically reviews tax rates to balance revenue collection with industry needs. In recent years, there have been discussions about potentially reducing GST on construction materials to boost the real estate sector. However, as of 2026, the rates mentioned above remain applicable.

Construction professionals should monitor GST Council decisions, as changes can significantly impact project economics. A reduction from 12% to 5% on any major material category would have immediate implications for ongoing and planned projects.

Digital Compliance and E-Invoicing

GST compliance has become increasingly digital. E-invoicing is now mandatory for most businesses, and this trend will continue strengthening through 2026. Ensure your suppliers provide e-invoices that can be uploaded to the GSTIN portal for proper ITC claims.

This digital infrastructure makes it easier to track GST paid and claimed, reducing compliance risks and enabling better project cost management.

Practical Tips for Managing GST on Construction Projects

Cost Optimization Strategies

1. Supplier Selection: Prioritize GST-registered suppliers to ensure ITC eligibility. When comparing quotes, always factor in GST differences. A supplier offering 5% lower prices but unregistered might actually cost more after accounting for reverse charge GST.

2. Material Specifications: Work with architects and engineers to specify materials that attract lower GST rates where functionally equivalent. For example, choosing standard tiles over decorative ones saves 7% in GST.

3. Timing of Purchases: Plan material procurement to align with project phases and ITC availability. Purchasing materials before you can claim ITC creates working capital pressure.

4. Documentation: Maintain meticulous records of all GST invoices and payments. Poor documentation can lead to ITC denials and compliance penalties.

5. Professional Guidance: For projects exceeding ₹1 crore, engage a GST consultant. The cost of consultation (typically ₹50,000-₹2,00,000) is easily recovered through proper ITC management.

Budget Allocation

When preparing construction budgets, allocate GST as follows:

Materials with 5% GST: Add 5% to base cost

Materials with 12% GST: Add 12% to base cost

Services: Add 5-12% depending on project value

Contingency: Add 2-3% for GST-related uncertainties

For a ₹1 crore project with typical material and service mix, GST typically adds ₹8-12 lakhs to the final cost. Accurate budgeting prevents cost overruns.

Finding GST-Compliant Suppliers and Professionals

Navigating GST compliance is easier when you work with professionals who understand the implications. AECORD connects you with verified suppliers, contractors, and consultants who are GST-registered and compliant. When sourcing materials and services through AECORD, you can be confident about GST registration status and invoice authenticity.

The platform's verification process ensures that suppliers meet GST compliance standards, reducing your risk of reverse charge complications or ITC denials. This is particularly valuable for architects and engineers managing multiple suppliers across different cities.

Conclusion

GST on construction materials in India 2026 continues to be a critical factor in project economics. While the 5% rate on essential materials like cement, steel, and bricks is favorable, the complexity of GST compliance requires careful planning and professional management.

Key takeaways for construction professionals:

Understand the specific GST rates for materials in your project

Prioritize GST-registered suppliers to maximize ITC benefits

Factor GST into project budgets with precision

Maintain detailed documentation for compliance

Consider professional GST consultation for large projects

Monitor GST Council decisions for rate changes

By implementing these strategies, you can optimize your construction project costs and ensure full GST compliance. Start by identifying reliable, GST-registered suppliers for your next project. Visit AECORD today to connect with verified construction material suppliers, contractors, and consultants who understand India's GST landscape and can help you navigate it efficiently. Whether you're based in Delhi, Mumbai, Bangalore, or any other Indian city, AECORD's network of professionals is ready to support your project's success.

Frequently Asked Questions

What is the GST rate on cement and concrete in India 2026?

Cement, including Ordinary Portland Cement (OPC) and Portland Pozzolana Cement (PPC), attracts 5% GST in India. Ready-mix concrete (RMC) also falls under the same 5% bracket, making these essential materials cost-effective for construction projects.

How much GST do I need to pay on steel and reinforcement bars?

Mild steel bars and reinforcement steel (rebar) attract 5% GST, while finished steel products and structural steel sections are taxed at 12% GST. The rate depends on the processing stage and type of steel product you're sourcing.

What are the five GST tax slabs for construction materials?

India's GST system has five tiers: 0% (raw minerals), 5% (essential materials like cement and bricks), 12% (paints, electrical fixtures, plumbing), 18% (premium materials like glass and decorative items), and 28% (luxury items like air conditioning equipment).

Which construction materials have 5% GST in India?

Materials with 5% GST include cement, bricks, tiles, certain steel products, and ready-mix concrete. This favorable rate applies to goods considered essential for construction and typically used by lower-income groups.

How much can I save with 5% GST versus 12% GST on cement purchases?

For a typical project purchasing 1000 bags of cement at ₹500 per bag, the GST difference between 5% and 12% results in savings of approximately ₹3,500—a significant amount for medium-sized construction projects.